--- the subscriber area has no ads and those above are not selected or endorsed by this site ---

Short Term Macro Update +2

13:09 01-May-26

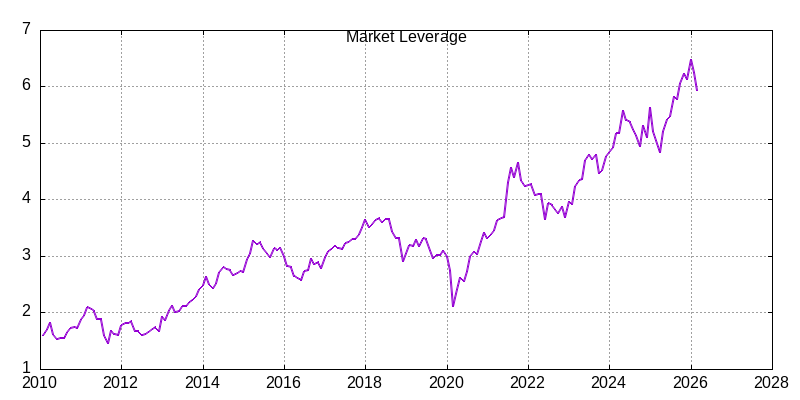

Market

leverage

in March dropped below 6x, which is still historically high, but

better than any level since September. This deserves to be

documented but ignored, given the war in the Middle East and

corresponding, temporary market dip. It's fair bet that it's right

back up again, and in keeping with the notes below, could stay that

way for months before there is a reckoning.

Market

leverage

in March dropped below 6x, which is still historically high, but

better than any level since September. This deserves to be

documented but ignored, given the war in the Middle East and

corresponding, temporary market dip. It's fair bet that it's right

back up again, and in keeping with the notes below, could stay that

way for months before there is a reckoning. In

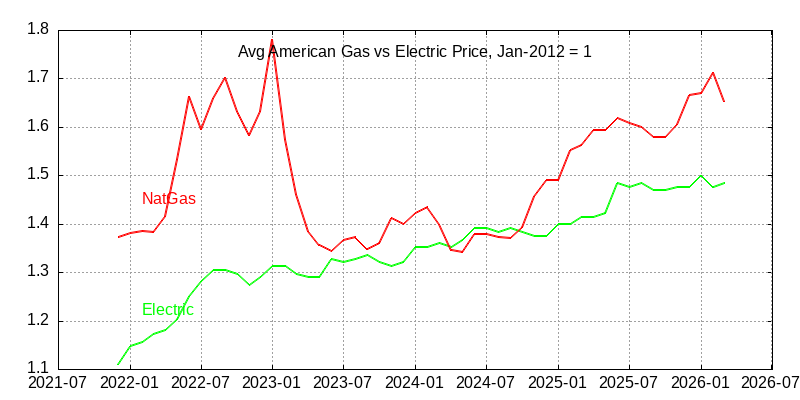

keeping with yesterday's PCE concern and the widespread outcry on

affordability, American natural

gas prices fell significantly in March, whereas the cost of electricity still

edged up slightly. Despite that, Maine's governor vetoed

the data center freeze that this service reported on a month ago, though it may

still return with an exemption for an existing project, which was

the governor's only objection. Growing opposition in other states

is also mentioned.

In

keeping with yesterday's PCE concern and the widespread outcry on

affordability, American natural

gas prices fell significantly in March, whereas the cost of electricity still

edged up slightly. Despite that, Maine's governor vetoed

the data center freeze that this service reported on a month ago, though it may

still return with an exemption for an existing project, which was

the governor's only objection. Growing opposition in other states

is also mentioned.On 5/1/26 11:06 AM, CrowdWisers

Administration wrote:

DHS is now funded, with the exception of ICE, which was in reality being funded all along. Even less importantly for the market, today marks the day when Trump should be seeking Congressional approval for Epic Fury. We can expect more federal dysfunction at least until November, and maybe beyond that, since yesterday's SCotUS decision makes it nearly impossible to mount a successful gerrymandering challenge. In the meantime, we can expect market indexes to keep hitting new highs at least while dollar weakness continues, or until some new real world event grabs public attention. One possibility for that is the worst local Linux exploit in years potentially allowing privilege escalation in virtual machine cloud environments.

Next week we're back to jobs data, in which ADP's weekly updates show a positive trend.