--- the subscriber area has no ads and those above are not selected or endorsed by this site ---

December CPI and Gemini Deal +3

15:14 14-Jan-26

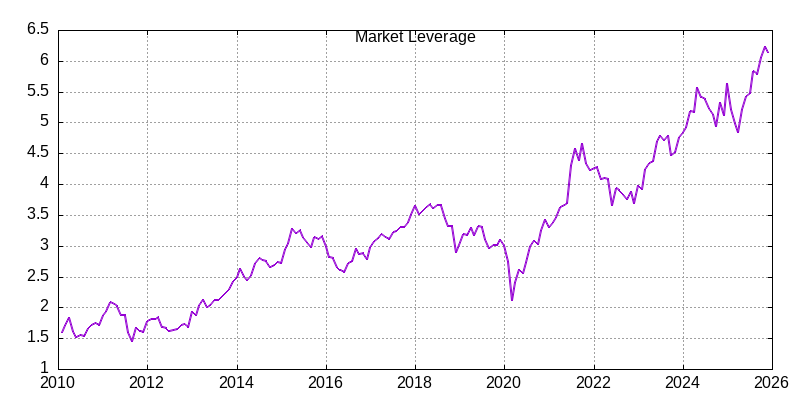

Market leverage

for December just came out, and it moderated slightly to 6.1x. This

is still unsustainable by historical standards, but it can be very

difficult to predict where it will end. I continue to expect that

the interplay with real estate will be important. My read is that

we're seeing more homes for sale, and I will continue to monitor the

official price and volume data going forward, with the next pending

home sales report due a week from today.

Market leverage

for December just came out, and it moderated slightly to 6.1x. This

is still unsustainable by historical standards, but it can be very

difficult to predict where it will end. I continue to expect that

the interplay with real estate will be important. My read is that

we're seeing more homes for sale, and I will continue to monitor the

official price and volume data going forward, with the next pending

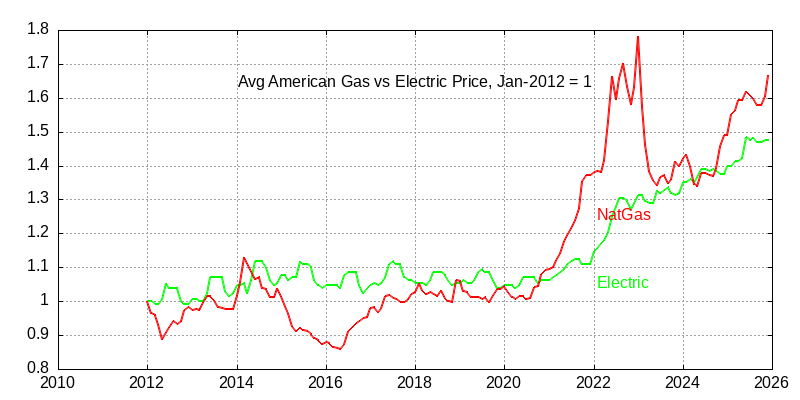

home sales report due a week from today. Data on natural

gas versus electricity pricing

has finally caught up, and though it shows the former spiking, we

already know that gas prices have plummeted by almost a third in the

new year. I would argue that the real thing to see here is the long

term and sequential rise both speaking to the affordability crisis

discussed below. Any attempt to address that will degrade the

current factors driving corporate profitability and thus stock

indexes.

Data on natural

gas versus electricity pricing

has finally caught up, and though it shows the former spiking, we

already know that gas prices have plummeted by almost a third in the

new year. I would argue that the real thing to see here is the long

term and sequential rise both speaking to the affordability crisis

discussed below. Any attempt to address that will degrade the

current factors driving corporate profitability and thus stock

indexes.Finally I will document that the October prices will never be reported, and thus show as flat for that month.

On 1/14/26 12:00 PM, Esekla wrote:

Despite American indexes being down, the stocks I track are mostly green today, led by SLB with media picking up on my note that it would be a prime candidate for a windfall from efforts to revitalize Venezuelan production... The rotation in today's trading seems emblematic of the media & market beginning to catch on to my peak Trump theme, which is supported by the pivot in his own rhetoric to acknowledge an affordability crisis, and big tech playing along. I would completely expect the hydrocarbon investors to be at the trailing end of that recognition.

Following up on yesterday's CPI report, there is a linger lack of confidence in the data and broad recognition that it will continue to be noisy for months, due to how analysis was handled following the federal shutdown. In light of that, this morning's delayed PPI report was not worth mentioning in real time, as it is dated and does nothing to change the narrative. What is worth mentioning is Miran's speech today, and how it highlights the importance of the battle over Fed independence. The governor is right about de-regulatory effects on productivity, but dead wrong about inflation, IMO. That will only be solved by reigning in graft and government spending, which means a functional Congress that can make smart compromises rather than playing politics.

On 1/13/26 9:19 AM, CrowdWisers

Administration wrote:

The December CPI report shows +0.3% for the headline and +0.2% for Core, with the former being in line and the latter a tenth below. Food has taken over as the primary source of trouble in living costs at +0.7%, but Shelter also remains stubbornly high at 0.4%. This is enough to produce a mildly positive reaction in American equity futures, but not enough to move the embattled Fed. I may follow up with commentary on how trustworthy this data is, but theorize that holiday retail competition helped. Regardless of the market response, it remains inconsistent with the Fed's bogus 2% inflation target.

Apple has struck a multi-year deal to use Gemini for Siri as anticipated in August. That has powered GOOG(L) shares to new all-time highs, and has as much to do with the positive macro rank on this note as CPI. AAPL shares are well off their early December highs, though. No price was disclosed, but it was rumored to be a billion dollar deal. Testing by our parent CrowdWisers service shows that Gemini on Android is no better than a web search and in some cases much worse. It also remains useless for device control. However, people do love natural language interfaces, and the AI trade still shows no sign of abating.