--- the subscriber area has no ads and those above are not selected or endorsed by this site ---

August CPI and AI update -3

16:03 16-Sep-25

Today's treasury auction saw stronger results than its predecessors, with a bid-to-cover ratio of 2.74, a high yield of 4.163%, and 92% of non-dealer bids accepted.

Also, here's the official swearing in notice from the Fed, which isn't supposed to care much about treasury sales, but this another data point that will help the hopes of those who want to hear a more dovish tone from the committee.

On 9/16/25 8:54 AM, CrowdWisers

Administration wrote:

It seems likely that both Cook and Miran will vote in tomorrow's FOMC decision. Last night, the D.C. circuit court of appeals upheld the injunction staying Cook's removal, and the Senate confirmed Miran to the Fed by a single vote. I have not seen evidence that the latter has been sworn in yet, but have little doubt that will happen this morning. He is also NOT leaving his post as head of the Council of Economic Advisers, but is taking unpaid leave. The dollar has weakened persistently and meaningfully against all major currencies since the week began, and this service may go back to monitoring treasury auction results, with the next one being 20-year bonds, scheduled for today.

On 9/15/25 9:25 AM, CrowdWisers Administration wrote:

Another Fed meeting is upon us, with the market more certain of what the decision will be than who will vote. It comes as no surprise that the administration appears to have inflated its case. Look for an update on the appeal of the injunction that confirmed Cook can stay at her post later today.

On the AI front, China is injecting more uncertainty with a short assertion that Nvidia has violated its antitrust laws (translation) without any accompanying detail. NVDA gapped down almost 1.7% to start pre-market trading below $175, but is already recovering, as the market recognizes sabre rattling on trade talks that are expected to conclude on the day of the Fed's press conference.

On 9/12/25 1:25 PM, CrowdWisers Administration wrote:

Analysis of bi-weekly census data has been drawing lots of commentary on peak AI already being here. I'm not a fan of surveys, but may look into graphing the data myself on an ongoing basis as a gauge of sentiment. A note on Nvidia scaling back its DGX data center aspirations amid corporate cost cutting doesn't help either.

I reiterate that I see the reality being a refinement of use cases featuring a slow migration to the edge, with management of personal devices as the killer app. This is because natural language interfaces offer a new front to both sides of the information economy. Users get to avoid searching endlessly for options that purveyors and governments prefer to hide, and then both sides get a new line of plausible deniability when regulators are eventually forced to look like as if something meaningful is being done again.

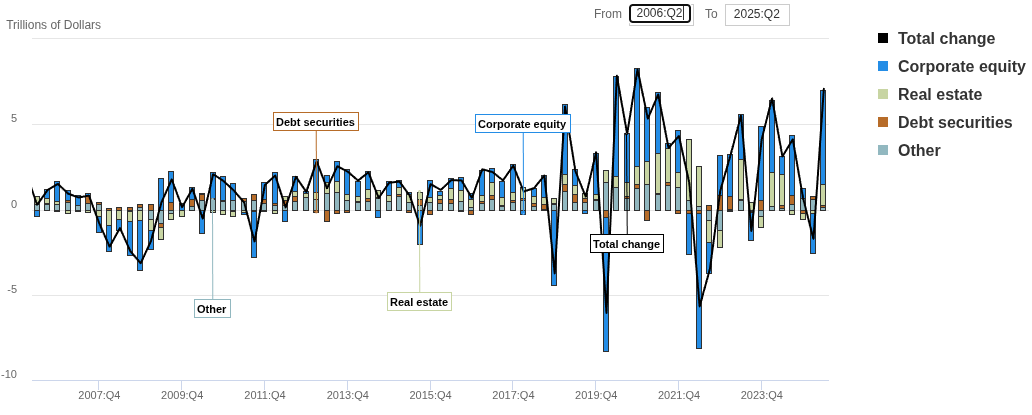

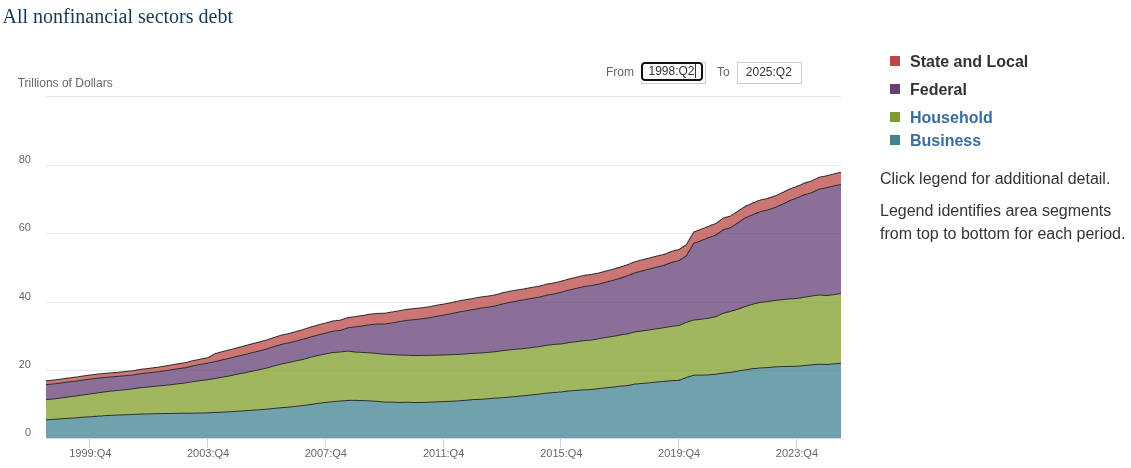

With aggregate numbers likely to hold up or even rebound, the AI hype cycle may not be done quite yet, but investors have seen the writing on the wall. So instead, have a look these two charts from the Fed's publication of Z1 accounts last night, showing the expanded role of equities in household finances, and how quickly they can turn.

Then consider that Federal debt has historically been less than both Household and Corporate debt, but it grew significantly after 2008 and the pandemic, now exceeding each by about half.

With world gradually shifting away from American dollar usage, that will complicate any bailout effort, supporting this service's prediction that stagflation is the best possible outcome.

.

On 9/11/25 2:33 PM, CrowdWisers Administration wrote:

Canada has publshed its initial 5 nation building projects under its One Economy legislation. The focus on physical infrastructure is quite pronounced, and it supports the general consensus that broadband over copper is no longer worth the effort. That has only grown in the wake of the EchoStar spectrum deals, where there is speculation that fixed wireless will be the only alternative to fiber and Verizon buy what's left. However, with the FCC having already dropped its inquiry, it appears that Ergen has already successfully called the regulator's bluff.

The opposite is true for Trump, who wound up trying to convince workers detained last week to stay in the country to train American workers. That makes raiding the site look like a bad move, as most of those detained entered the country legally, and merely had work violations or had overstayed their visas do to renewal processing delays. Korea's president declined the offer and said that such actions will only deter foreign investment in America.

On 9/11/25 9:02 AM, CrowdWisers Administration wrote:

August CPI numbers were just released with a headline that was a tenth higher than expected at +0.4%. Core was in line at +0.3%. Shelter and food were the largest contributors, though there was also a rebound in energy prices. All of this is consistent with the long term view expressed here that the Fed has no good options, but will choose to support a weakening job market. FedWatch chances for a half point rate cut topped out in the low teens after the employment reports, but now show just over 5%. Currencies are showing dollar strength, which leads me to believe that even though jobs didn't have a lasting impact the indexes, because markets only care how rich people are doing, a fade here could prove more persistent.

It's looking increasingly like the megacaps have nobody but each other to compete with. I'm hearing opinions that unlike a year ago, where we saw a crappy upgrade cycle for Google, the move to TSMC's leading edge node for its TPUs represents a first step toward real competition with Nvidia. The key difference here in my eyes is that, unlike AMD, Google has the software clout to compete even without a hands down performance lead. That should be another factor leading to reduced margins for both companies over time. For years, I've referenced AWS as competing mainly on price and flexibility, but Amazon is hitting back at Google by expending its advertising capabilities even further via a partnership with Netflix. Amazon is also making moves to compete in software-defined and autonomous vehicles.

I'm still never buying another Pixel phone, but I do think that a natural language interface to personal devices, including cars can be a killer app. It remains to be seen if the functionality is really there, and these trends will take at least another quarter to show up in corporate numbers, and thus indexes. Yet after many months of arguing that the major market trouble this service predicted years ago was still a long way off, we now appear to close to a major inflection point. Moving one level down the food chain, Oracle slips in under the wire with a capital raise for Perplexity valuing it at $20b. The resultant jump in ORCL by over a third shows that market euphoria continues for the time being.

My continued testing of Perplexity and other major genAIs hasn't changed the conclusion I reached last November:

All of these companies continue investing heavily in AI, but profitable results beyond specific technical use cases are uncertain, to put it kindly; a cynic might claim that the optimism we've seen to date is simply due to most humans being unable to differentiate smooth language from actual intelligence.Although natural language can be better than simple search terms in some cases, all of them show severe limitations in performing tasks that require even basic logic and lie incessantly. This makes their results worthless without checking sources, which they are often opaque about. Per the notes in the prior paragraph, none of that makes them worthless, but overvalued would not be too strong a word. Ultimately, I think we'll wind up finding out how much customers just want something to talk to.